The cost of renting in many areas is now greater than the cost to buy. Even with mortgage rates on the rise, it is still more affordable than renting. Some say mortgage loans are impossible to obtain without perfect credit and/or 20% down.

Want the truth? Read on, and we’ll cite the three basic factors for qualifying for a home loan.

Income – If you have a job or steady source of income, you’re off to a great start. If you’re already able to pay your rent on time each month, this could actually be easier than you might think.

Assets – You rarely need a 20% down payment. In reality, many programs will work with 5%, 3.5% or 3%, and in some cases, even 0% down. As well, closing costs can sometimes be paid by lenders, sellers or come from gifts or grants. So if you think you’re out of luck just because you don’t have tons of cash, no worries. Chances are still good there’s a solution that may work.

Credit – Your credit is likely in good shape if you pay your bills on time and have avoided major issues like bankruptcy, foreclosure, short sales and judgments. Requirements will always vary, but there can still be reasonably flexible loan options, such as the FHA and Fannie Mae which both allow for low credit scores.

That’s it. These three items are the fundamentals of mortgage lending. Exceptions will exist, but don’t be fooled into thinking the process is impossible. For those who work and pay their bills, there may not be a whole lot standing in the way of homeownership.

Here is an example of Buying a home vs. Renting based on today’s mortgage rates with the plan of selling your home in 10 years.

Renting versus Owning

I would like the opportunity to consult with you and start you on the path of Homeownership. Whether it be for Today or planning for Tomorrow!

Bill Nickerson NMLS #4194 | 978.273.3227 | Email | Website

An Adjustable Rate Mortgage provides a specific fixed rate term before becoming an adjustable mortgage. An example: A 10/1 ARM is fixed for the first 10 years and then becomes a 1 year adjustable rate for the remaining term of the mortgage, thus giving you 10 years of security at a fixed rate.

Advantages: If you know that you are selling your home in a short period of time, 10-12 years or less, you can get a mortgage rate that is 3/4’s to 1 full percent below the traditional mortgage rates. Today a 10 year ARM is 5.00% and you can borrower up to 2 Million Dollars.

How do they work?

Adjustable Rate Mortgages (ARM’s) come in many different varieties. The most common ARM’s are the following: Three Year, Five Year, Seven Year and a Ten Year. You will also see them displayed in this format as well: 3/1, 5/1, 7/1 and 10/1. The first number represents the amount of years the loan will be fixed for and will not change from its original start rate. The higher the first number or term, the higher the interest rate will be.

The second number represents how often the ARM will adjust after the fixed rate term ends. Using a 5/1 ARM as the example, when your fixed term is about to expire, the Lender will send you a notice via mail notifying you that your rate is about to adjust and what that adjustment will be. This will occur 45 days prior to this expiration date, in this case that would be 60 months in to this loan (5 Years). The new rate will be set for one year, or the term that is stated in the second number, 5/1.

The adjustments are based on 2 variables, the index and the margin. The margin is set on the day you get the mortgage and is usually in the range of 2.25 or 2.75 depending upon the type of ARM you go with. This will never change and is set for the life of the loan. We would then add the current Index to this margin and combined that would create your new rate.

The Index can come from many places but is selected when we lock in your loan. Typically we use the One Year Treasury Bill or the One Year LIBOR. Both indexes move fairly slowly. These Indexes are always posted in the Wall Street Journal but is very easy just to Google these terms. This will show you the current rate as well as show the history of these rates. You can also click this site at the US Treasury

Today’s one year treasury is at 4.00 (9/16/2022), this is the index. Add this to the margin of 2.50 and your new rate today would be 6.50%. This is know as the Fully Indexed Rate. This rate would be rounded up to the next highest/nearest 1/8th in the case the T-Bill was not an even number. Remember, this is what the rate would adjust to after the fixed term has ended.

Caps: Your loan comes with caps of 5/2/5, each number represents how your loan will adjust. With the first adjustment the loan can adjust 5% up or down from the original start rate. The second number “2” is what it can adjust each time for the remaining years of the loan. So, the second adjustment and every one after that the rate can move up or down a maximum of 2%. The last number is the Life Cap. This rate will never go higher than 5% of the starting rate. So if you lock in a rate of 5.00% today, your rate would never exceed 10.00%. To give you an idea, since 1996, this rate has not exceeded 8.25% at its high point. In the last several years, this rate as adjusted downward and as low as 2.00% in many cases.

I hope this is helpful. Always feel free to ask questions about any of this information. Email me at Bill@billnickerson.com or call 978-273-3227.

Thank you very much,

Bill Nickerson NMLS# 4194 | Mortgage Equity Partners| Lynnfield MA

The Federal Reserve System (also known as the Federal Reserve or simply the Fed) is the central banking system of the United States of America. It was created on December 23, 1913, with the enactment of the Federal Reserve Act, after a series of financial panics (particularly the panic of 1907) led to the desire for central control of the monetary system in order to alleviate financial crises. Over the years, events such as the Great Depression in the 1930s and the Great Recession during the 2000s have led to the expansion of the roles and responsibilities of the Federal Reserve System.

In the movie, It’s A Wonderful Life, George Bailey’s Bank experiences a financial crisis causing a panic and his deposit customers demanding to withdraw all of their funds, otherwise known as “A Run on the Bank”.

George Bailey trying to prevent a “Run on the Bank”

What is the Fed Fund Rate?

In the United States, the federal funds rate is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight, on an uncollateralized basis. Reserve balances are amounts held at the Federal Reserve to maintain depository institutions’ reserve requirements. Institutions with surplus balances in their accounts lend those balances to institutions in need of larger balances. The federal funds rate is an important benchmark in financial markets. (This is so a “Run” on the bank will never occur again)

The interest rate that the borrowing bank pays to the lending bank to borrow the funds is negotiated between the two banks, and the weighted average of this rate across all such transactions is the federal funds effective rate. The federal funds target rate is determined by a meeting of the members of the Federal Open Market Committee which normally occurs eight times a year about seven weeks apart. The committee may also hold additional meetings and implement target rate changes outside of its normal schedule.

When a Bank gets in to trouble and does not have enough funds to operate, they are allowed to borrow money from the Federal Reserve or from another Bank, the rate that is used is the Federal Fund Rate and is solely used for overnight lending from bank to bank. This rate has been adopted by several other indexes and rates.

The Fed Fund Rate is also used to set other Rates, the majority being adjustable rates. Mortgage rates are influenced by the Fed Fund Rates but do not use this index to adjust.

What Rates are based on the FED FUND RATE?

Since the time of the Federal Fund Rate was introduced, other rates have been formulated or calculated using this rate as the base rate. It is typically adjustable rates that are used for setting the Prime Rate, Credit Card Rates, Home Equity Lines of Credit to name a few. In the example of the Prime Lending Rate, the rate uses the Fed Fund Rate plus a margin of 3% to create the Prime Rate. Credit Cards HELOC’s will use the Prime Rate as its base and then add a margin to that rate for the banks profit margin. The Federal Reserve uses open market operations to make the federal funds effective rate follow the federal funds target rate. The target rate is chosen in part to influence the money supply in the U.S. economy.

Mortgage Rates are indirectly influenced by Federal Reserve by changing its target for the federal funds rate. This latest increase by the Feds on July 27th, 2022, actually caused mortgage rates to decrease. For more information on what makes mortgage rates adjust, click here: Why do mortgage rates change so much?

George Bailey trying prevent panic at Baileys Savings and Loan

Financial institutions are obligated by law to maintain certain levels of reserves, either as reserves with the Fed or as vault cash. The level of these reserves is determined by the outstanding assets and liabilities of each depository institution, as well as by the Fed itself, but is typically 10% of the total value of the bank’s demand accounts (depending on bank size). In the range of $9.3 million to $43.9 million, for transaction deposits (checking accounts, NOWs, and other deposits that can be used to make payments) the reserve requirement in 2007–2008 was 3 percent of the end-of-the-day daily average amount held over a two-week period. Transaction deposits over $43.9 million held at the same depository institution carried a 10 percent reserve requirement.

For example, assume a particular U.S. depository institution, in the normal course of business, issues a loan. This dispenses money and decreases the ratio of bank reserves to money loaned. If its reserve ratio drops below the legally required minimum, it must add to its reserves to remain compliant with Federal Reserve regulations. The bank can borrow the requisite funds from another bank that has a surplus in its account with the Fed. The interest rate that the borrowing bank pays to the lending bank to borrow the funds is negotiated between the two banks, and the weighted average of this rate across all such transactions is the federal funds effective rate.

U.S. Federal Reserve Chairman Jerome Powell

The federal funds target rate is set by the governors of the Federal Reserve, which they enforce by open market operations and adjustments in the interest rate on reserves. The target rate is almost always what is meant by the media referring to the Federal Reserve “changing interest rates.” The actual federal funds rate generally lies within a range of that target rate, as the Federal Reserve cannot set an exact value through open market operations.

Another way banks can borrow funds to keep up their required reserves is by taking a loan from the Federal Reserve itself at the discount window. These loans are subject to audit by the Fed, and the discount rate is usually higher than the federal funds rate. Confusion between these two kinds of loans often leads to confusion between the federal funds rate and the discount rate. Another difference is that while the Fed cannot set an exact federal funds rate, it does set the specific discount rate.

The federal funds rate target is decided by the governors at Federal Open Market Committee (FOMC) meetings. The FOMC members will either increase, decrease, or leave the rate unchanged depending on the meeting’s agenda and the economic conditions of the U.S. It is possible to infer the market expectations of the FOMC decisions at future meetings from the Chicago Board of Trade (CBOT) Fed Funds futures contracts, and these probabilities are widely reported in the financial media.

For more information about the Federal Reserve, The Markets and Mortgage Information; please email, call or text anytime.

Find out how to build credit and maintain a healthy credit score with help from Mortgage Equity Partners.

Keeping a healthy credit score is integral to maintaining your financial wellness and moving toward your life goals.

And if your credit score isn’t quite where you want it to be, the good news is that it’s not set for life; your credit score can always improve with the help of smart financial practices. If you’re looking for ways to build and maintain a healthy credit score, take action with these tips.

1.Stay on top of your bills.

While it might sound obvious, you need to pay your bills on time, every time. This is one of the simplest ways to build credit, as it shows lenders that you are a responsible borrower. Making timely payments has a positive impact on your credit score, so be sure to stay on top of deadlines or set up an auto-pay system for your accounts. Remember, your bill payment history accounts for approximately 35% of your credit score, and even just one late payment can leave a negative mark.1

2. Keep track of spending.

Budgeting is important in any financial situation, but it’s especially helpful when it comes to managing your credit cards. If you start to see that your monthly spending is getting close to your credit limit, it may be a good idea to increase your limit or consider scaling back on expenses. Your credit utilization ratio (how much available credit you actually use) has an impact on your credit score. Utilizing a small portion—we recommend 30% or less—of your available credit will go a long way in strengthening your score.

3. Pay off debts quickly.

According to a NerdWallet study, the 2018 average total of credit card debt owed by a U.S. household was $6,803. If you’ve missed any payments in the past, your credit score has probably dipped a little; however, you can minimize the impact of that debt by paying it down quickly. Get back on track by cutting out unnecessary expenses and creating a payment plan. A good credit building practice is to never borrow more than you are able to pay back. Ultimately, the amount of debt you carry matters as it determines about 30% of your credit score.1

4. Diversify the credit you use.

Having a solid credit mix plays a positive role in your credit health, demonstrating your ability to manage multiple types of debt at the same time. It’s not necessary to have each one, but a mix of credit cards, retail accounts, installment loans, mortgage loans, and student loans may help improve your score. Evaluate the different types of credit you have open and make sure it’s a healthy mix of open and closed-end credit. Open-end credit refers to any loan where you can make repeated withdrawals and repayments, like a credit card. Closed-end credit refers to a loan that is fixed for a period of time with regular payments, like a car loan or mortgage. Your credit mix accounts for approximately 10% of your credit score.1

5. Try a credit monitoring service.

Credit monitoring services such as Privacy Guard, Credit Karma, and Identity Force are designed to help protect you from identity theft by keeping a close watch on your credit report. After signing up for a service, they watch over your credit activity and alert you of any changes to your accounts, helping you avoid fraud and identity threats. This is especially important because the Identity Theft Resource Center (ITRC) uncovered that the number of credit card numbers exposed in 2017 totaled 14.2 million, which was up 88% from the previous year.2 Some services even offer personalized advice on how to maintain a healthy score. Monitoring your report may not be an instant way to build credit, but being proactive can help you quickly identify and solve potential threats before they have a chance to hurt your credit score.

6. Be patient.

The length of your credit history makes up about 15% of your credit score.1 Depending where you are on your credit journey, it will take some time to age your credit history. In the meantime, focus on your financial habits and see where improvements can be made. Paying bills on time every time, paying off debts, keeping track of spending, and routinely monitoring your credit are all great ways to build credit over time.

Continue your credit journey.

if you ever have any questions on how to build credit or keep up positive financial habits. We can walk you through actionable steps to improve your existing plans, or help you get started.

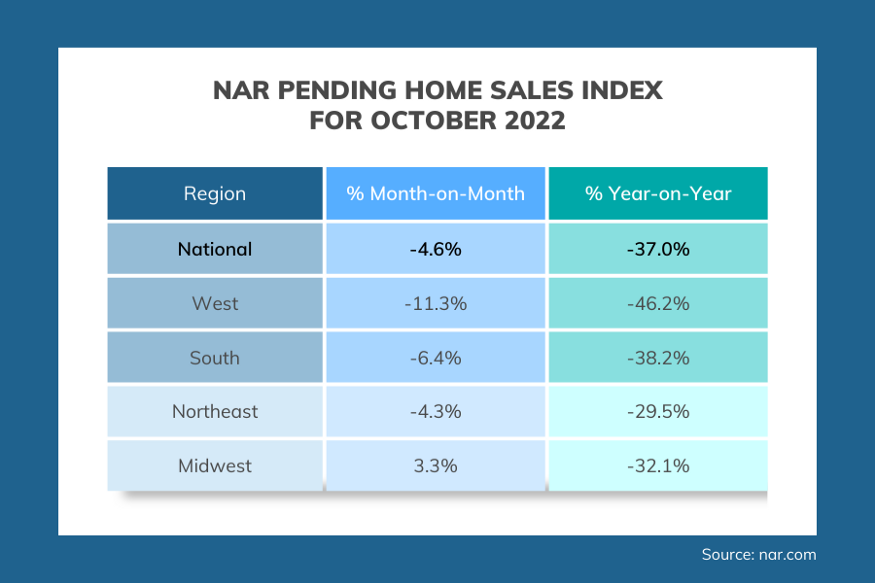

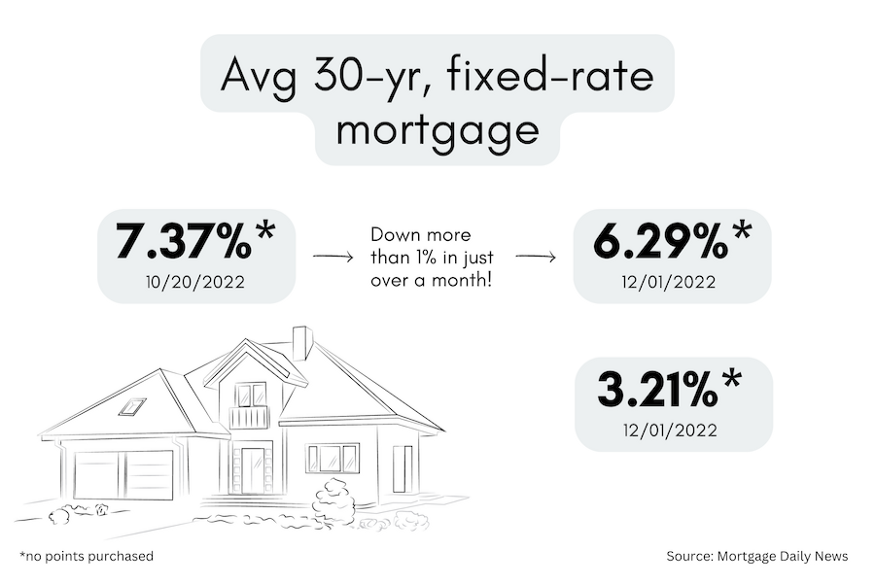

The NAR’s Pending Sales Index for October fell 4.6% in a month and 37% compared to October 2021. Pending sales in the West region were down 46%. [Source: NAR] Keep in mind that 30-yr mortgage rates were >7% for the entire month of October. They’re now around 6.3%.

The Case-Shiller Home Price Index for September fell 1% in a month. From their peak in June, national home prices have slid ~2.5%, while prices in SFO & SEA are now down more than 10%. [Source: CoreLogic]

Fed Chair Jerome Powell said that “the time for moderating the pace of rate increases may come as soon as the December meeting” during a speech at the Brookings Institution. In other words, no more +75 bps.

The day after Powell’s comments, the PCE inflation figure for October came in at an annualized rate of 6%, better (that is to say, lower) than expectations and a further deceleration from 6.3% in September and the peak of 7% in June. [Source: BEA]

Companies added only 127k jobs in November, vs. +239k in October. This was well below Street expectations. Job losses in manufacturing & biz services dragged the total lower. [Source: ADP]

The NAHB’s Chief Economist expects a mild recession from 4Q 2022–2Q 2023, but sees mortgage rates at or below 6% by end-2023/early 2024, either because the Fed has ‘beaten’ inflation, or because the recession turns out to be bigger than expected. [Source: NAHB]

Pending Sales for October

With 30-year mortgage rates above 7% for the entire month, we knew that October pending sales would be bad — and they were. The NAR’s Pending Home Sales Index (PHSI) dropped 4.6% in a month. That’s the 5th-straight monthly decline in the PHSI. Compared to October 2021, the PHSI was down 37% YoY.

The contraction was significantly worse in the West, with October pending sales dropping 11% MoM and down 46.2% YoY. That’s right, pending sales nearly halved in the West.

Pending sales are a forward indicator of existing home sales (leading by 1–2 months). So prepare yourself for some nasty November and December existing home sales figures.

But there’s a silver lining: mortgage rates are already 90–100bps (a full percentage point) lower. As NAR’s Chief Economist Lawrence Yun wrote, “October was a difficult month for buyers as they faced 20-year-high mortgage rates…[but] The upcoming months should see a return of buyers as mortgage rates appear to have already peaked and have been coming down since mid-November.”

In fact, there are signs that a recovery in activity (thanks to lower rates) is already happening. The MBA (Mortgage Bankers Association) tracks new purchase loan applications on a weekly basis. This is the fourth week in a row that applications have risen week-on-week.

Case-Shiller for September

For the third consecutive month, home prices declined on a month-over-month basis. The national index was down 1.0% MoM, but the 20-city index was down 1.5% MoM. Don’t be fooled by the small numbers; these are big decreases. If this happened every month, prices would be down 12–18% in a year.

As in August, prices declined in each of the 20 big cities. However, for the cities experiencing the sharpest price drops (San Francisco, Seattle, Las Vegas etc.), the magnitude of price declines actually slowed a bit in September.

Source: S&P CoreLogic Case-Shiller Index

NAHB Webinar

Here’s how the National Association of Homebuilders’ Chief Economist, Robert Dietz, sees things:

2020–2021: Unsustainable, above-trend growth in home sales 2022–2023: Compensating below-trend growth in home sales 2024+: A return to trend growth in home sales (with >1 million in new home sales annually)

He expects a mild recession for the next three quarters, unemployment rates rising to near 6% (from 3% today) in 2024 and national home prices falling ~10%. At the same time, his message was essentially optimistic — lower inflation, interest rates and home prices will bring buyers (and builders) back relatively quickly.

A few anecdotes I found interesting:

~50% of the webinar attendees (most of whom were builders) said that they were responding to slowing demand with either price cuts OR enhanced incentives

The construction industry needs ~750,000 new workers every year to keep pace with demand and replace retirees

Right now, two cities in Texas (Houston and Dallas) are adding more new homes than the entire state of California

Note: In any given year, existing home sales are 7–15 times higher than new home sales. This isn’t because builders are lazy. It’s because there are around 145 million existing housing units. Even if builders were able to construct 2 million homes a year (something they’ve never achieved before), that would only raise the total housing stock by 1.3%.

Mortgage Market

After months of extreme volatility, 30-yr mortgage rates had flatlined at 6.6% for several weeks. But with another good (well, improving) inflation figure, and Powell sounding a bit less hawkish, the bond market was in party mode yesterday, rising 70–80 basis points.

Higher mortgage bond prices = lower mortgage bond yields = lower mortgage rates. Yesterday, the 30-yr mortgage rates moved sharply lower to 6.3% — that’s a full percentage point lower than the peak of 7.37% on October 20!

They Said It

“When home prices decline, it’s pretty rare for there to not be a recession.” — NAHB Chief Economist Robert Dietz

“To anyone with a sense of history, the home boom must be a source of wonder. Housing usually leads the economy into a recession. Mortgage rates rise, then housing construction and home sales fall.” — Robert J. Samuelson in a 2002 Newsweek article

Inspiration

There are many different approaches to measure ‘affordability.’ But they all depend on three factors: 1) household income, 2) home prices, and 3) mortgage rates.

Right now, all three factors are moving in buyers’ favor:

Workers are getting paid more

Home prices are starting to slide

Mortgage rates have peaked

Plus, there are more homes available, and less competition than last year, and sellers are more willing to negotiate on things like repairs, covering some closing costs, paying for points etc.

This artitcle is written by Scott Bradley Brixen who writes for Listreports.com

Scott Bradley Brixen A CFA with 20 years of experience in global investment banking and equity research, ListReports’ “Eclectic Economist” finds everything interesting.

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses.”

These words in addition to the 8 minute speech, tanked the stock market and caused mortgage rates to go up since Friday, August 26th.

Federal Reserve Chairman Jerome Powell: Thank you for the opportunity to speak here today.

Jerome Powell

At past Jackson Hole conferences, I have discussed broad topics such as the ever-changing structure of the economy and the challenges of conducting monetary policy under high uncertainty. Today, my remarks will be shorter, my focus narrower, and my message more direct.

The Federal Open Market Committee’s (FOMC) overarching focus right now is to bring inflation back down to our 2 percent goal. Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all. The burdens of high inflation fall heaviest on those who are least able to bear them.

Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.

The U.S. economy is clearly slowing from the historically high growth rates of 2021, which reflected the reopening of the economy following the pandemic recession. While the latest economic data have been mixed, in my view our economy continues to show strong underlying momentum. The labor market is particularly strong, but it is clearly out of balance, with demand for workers substantially exceeding the supply of available workers. Inflation is running well above 2 percent, and high inflation has continued to spread through the economy. While the lower inflation readings for July are welcome, a single month’s improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down.

We are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2 percent. At our most recent meeting in July, the FOMC raised the target range for the federal funds rate to 2.25 to 2.5 percent, which is in the Summary of Economic Projection’s (SEP) range of estimates of where the federal funds rate is projected to settle in the longer run. In current circumstances, with inflation running far above 2 percent and the labor market extremely tight, estimates of longer-run neutral are not a place to stop or pause.

July’s increase in the target range was the second 75 basis point increase in as many meetings, and I said then that another unusually large increase could be appropriate at our next meeting. We are now about halfway through the intermeeting period. Our decision at the September meeting will depend on the totality of the incoming data and the evolving outlook. At some point, as the stance of monetary policy tightens further, it likely will become appropriate to slow the pace of increases.

Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy. Committee participants’ most recent individual projections from the June SEP showed the median federal funds rate running slightly below 4 percent through the end of 2023. Participants will update their projections at the September meeting.

Our monetary policy deliberations and decisions build on what we have learned about inflation dynamics both from the high and volatile inflation of the 1970s and 1980s, and from the low and stable inflation of the past quarter-century. In particular, we are drawing on three important lessons.

The first lesson is that central banks can and should take responsibility for delivering low and stable inflation. It may seem strange now that central bankers and others once needed convincing on these two fronts, but as former Chairman Ben Bernanke has shown, both propositions were widely questioned during the Great Inflation period.1 Today, we regard these questions as settled. Our responsibility to deliver price stability is unconditional. It is true that the current high inflation is a global phenomenon, and that many economies around the world face inflation as high or higher than seen here in the United States. It is also true, in my view, that the current high inflation in the United States is the product of strong demand and constrained supply, and that the Fed’s tools work principally on aggregate demand. None of this diminishes the Federal Reserve’s responsibility to carry out our assigned task of achieving price stability. There is clearly a job to do in moderating demand to better align with supply. We are committed to doing that job.

The second lesson is that the public’s expectations about future inflation can play an important role in setting the path of inflation over time. Today, by many measures, longer-term inflation expectations appear to remain well anchored. That is broadly true of surveys of households, businesses, and forecasters, and of market-based measures as well. But that is not grounds for complacency, with inflation having run well above our goal for some time.

If the public expects that inflation will remain low and stable over time, then, absent major shocks, it likely will. Unfortunately, the same is true of expectations of high and volatile inflation. During the 1970s, as inflation climbed, the anticipation of high inflation became entrenched in the economic decision making of households and businesses. The more inflation rose, the more people came to expect it to remain high, and they built that belief into wage and pricing decisions. As former Chairman Paul Volcker put it at the height of the Great Inflation in 1979, “Inflation feeds in part on itself, so part of the job of returning to a more stable and more productive economy must be to break the grip of inflationary expectations.”2

One useful insight into how actual inflation may affect expectations about its future path is based in the concept of “rational inattention.”3 When inflation is persistently high, households and businesses must pay close attention and incorporate inflation into their economic decisions. When inflation is low and stable, they are freer to focus their attention elsewhere. Former Chairman Alan Greenspan put it this way: “For all practical purposes, price stability means that expected changes in the average price level are small enough and gradual enough that they do not materially enter business and household financial decisions.”4

Of course, inflation has just about everyone’s attention right now, which highlights a particular risk today: The longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched.

That brings me to the third lesson, which is that we must keep at it until the job is done. History shows that the employment costs of bringing down inflation are likely to increase with delay, as high inflation becomes more entrenched in wage and price setting. The successful Volcker disinflation in the early 1980s followed multiple failed attempts to lower inflation over the previous 15 years. A lengthy period of very restrictive monetary policy was ultimately needed to stem the high inflation and start the process of getting inflation down to the low and stable levels that were the norm until the spring of last year. Our aim is to avoid that outcome by acting with resolve now.

These lessons are guiding us as we use our tools to bring inflation down. We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored. We will keep at it until we are confident the job is done.

1. See Ben Bernanke (2004), “The Great Moderation,” speech delivered at the meetings of the Eastern Economic Association, Washington, February 20; Ben Bernanke (2022), “Inflation Isn’t Going to Bring Back the 1970s,” New York Times, June 14. Return to text

3. A review of the applications of rational inattention in monetary economics appears in Christopher A. Sims (2010), “Rational Inattention and Monetary Economics,” in Benjamin M. Friedman and Michael Woodford, eds., Handbook of Monetary Economics, vol. 3 (Amsterdam: North-Holland), pp. 155–81. Return to text

The overall costs of Lending has been on the rise for the last several months. With the latest Inflation Rate of 9.1%, this will cause the Federal Reserve to raise rates again and most likely more aggressively than previous rate hikes.

We have come up with a SPECIAL program to relieve this stress! You can now LOCK in to Today’s Mortgage Rate while you are shopping for a home. This allows you to shop up to 90 Days with the security of knowing you are locked in.

This program is good for Fannie Mae and Freddie Mac loan limits in your area. Here is a link to the Fannie Mae Loan Limits in your Area. Depending upon the County you are in will determine the maximum loan amount for this program.

For more information on this program, feel free to call or email me anytime!

We have been spoiled with mortgage rates over the last few years as we saw the the 30 Year Fixed Rate get to the 2.50% range. As we move forward in 2022, mortgage rates have already started to climb. Rates are in the 4.00% to 4.25% range and we now have to adjust our purchasing power. Each half of a percent (.50%) in mortgage rate equates to about $25,000 of buying power. Depending upon when you were “Pre-Approved” for a mortgage, the new rates may greatly affect the home you now qualify for.

What should you do? Call your Lender or Bank and have your “Pre-Approval” updated to reflect the current mortgage rate of today. This will bring your purchase price and loan amount down as these higher rates will increase the overall cost of your mortgage payment.

Why is this happening? When the Fed raises the federal funds target rate, the goal is to increase the cost of credit throughout the economy. Higher interest rates make loans more expensive for both businesses and consumers, and everyone ends up spending more on interest payments.

Those who can’t or don’t want to afford the higher payments postpone projects that involve financing. It simultaneously encourages people to save money to earn higher interest payments. This reduces the supply of money in circulation, which tends to lower inflation and moderate economic activity—a.k.a. cool off the economy.

Economists have been warning us for the last few years, mortgage rates have to go up! The longer you wait, the more it will cost to buy a home. Or another way to look at this, you buying power could drop by 10% or more for each 1% increase in mortgage rate. Buy now while the mortgage rates are still low as we may not see these rates again in our lifetime!!

For more information on Mortgage Rates and Programs, feel free to call or email me anytime.

Have you ever called a mortgage company and received a quote and then called back the next day and the same rate was no longer available??

Mortgage companies, Banks and Credit Unions are subject to potential daily and even hourly shifts in the market. Interest rates fluctuate on the simple principal of supply and demand.

Mortgage rates trade based on Mortgage Back Securities and The Bond Markets as well as the overall economy. The vehicles that mortgage rates are based on are considered very conservative, stable and tend not to have the wild swings that one would find in the Stock Market. If the Stock market begins to see large increases or decreases, Investors will shift Billions of dollars in and out of the Stock Market and move them in to the Mortgage Markets. This will cause mortgage rates to either rise or fall. Stock Market tanks, good news for Mortgage Rates, Stock Market rallies and rates suffer. Investors and Traders will constantly shift funds out of the riskier stocks into the safe haven of the mortgage markets. These shifts can occur as little as once a day or in some cases can happen multiple times during a trading day. Thus causing mortgage rates to possibly change multiple times in a day.

These markets are affected globally as well; so even after the markets are closed in US, whatever is happening in Europe, Asia and around the world will cause our markets to move one way or the other.

Here are some of the variables that are being watched in today’s market:

Covid-19 – Global Pandemic

Ukraine

Europe and Asia’s Economy

Comments by the President

Politics

The US Housing Market

Unemployment in our Country

The Price of Oil and Gas

The “Feds” decision to move short term interest rates

The overall health of the US Economy

Any of these items can trigger a rally one way or another. Even a simple comment at a breakfast meeting by the President, the Fed Chairman or someone in power is enough to influence the markets.

Additional Mortgage Rate and Index Information:

To help us understand why mortgage rates change, it is important to realize that there is not one interest rate, but multiple ones. Below are some of the most prevalent interest rates and indexes that also have an impact on mortgage rates:

Prime rate – This rate is often offered to a bank’s best customers. If you are shopping for a home equity line of credit, then it is important to familiarize yourself with the prime rate. HELOCs are typically based upon the prime rate -plus or minus a certain percentage.

LIBOR – Stands for London Inter-bank Offered Rates. Libor rates are based upon the rates that a select group of London Banks offer each other for inter-bank deposits. Many adjustable rate mortgage programs use the Libor index.

Treasury bill rates”T-bills” and Treasury Notes – These are short-term and intermediate debt instruments used by our Government to finance their debt. The treasury index is based upon the auctions of U.S. Treasury bills or on the Treasury’s yield curve. Like the LIBOR index, the U.S. Treasury index is a popular index for adjustable rate mortgage products. Also, the Twelve Month Treasury Average (12 Month MTA) is a popular index which is based upon the twelve month average of the monthly yields of U.S. Treasury securities (maturing in one year). The MTA is a popular choice for option arm mortgage programs.

Treasury Bonds – Unlike T-bills and Treasury Notes, treasury bonds are long-debt instruments. These bonds are used by the U.S. Government to finance its debt.

Cost of Savings Index – often referred to as the COSI index. This index is based upon the annual average of interest rates on World Savings deposit accounts. The average is pulled on the last day of each month.

11th District Cost of Funds – Often referred to as the COFI index – The COFI index is based upon the average of the borrowing cost to member banks of the Home Loan Bank of San Francisco of the 11th District. Unless you are shopping for an option arm mortgage, it is unlikely that your loan will be affected by this rate.

Certificates of Deposit Index – Often referred to as the CODI index – this index is arrived at by calculating the average of the past twelve months rates of 3 month CD rates.

Federal Funds Rate – The fed funds target rate is the rate which federally chartered banking institutions lend balances to other depository banks overnight.

This is a lot of information to weigh each day when calculating mortgage rates. In general, most Banks, Investors, Lenders etc. will set rates around 10:30am once most of the morning economic reports have been released and the markets have had time to react to the information. In a calm trading day on Wall Street, these rates would be good for that day. In a day where lots of Economic reports and World events are occurring, these rates can be reset a few times as the Markets fluctuate. It is important to call your lender or bank often to check on these rates as they can and will change. It also important not to follow online rate sites that may be posting Average Rates as this information can be old as well a different Financial Picture then you may have. The Freddie Mac rates are based on closed loans from last week and an average of .7 Points of fees in the rate. This may give you a range, but not accurate enough to base your mortgage payment on or what is happening today in the markets.

Bill Nickerson has been in the Mortgage industry since 1991. Please leave a comment, email or call me anytime with questions you may have about mortgage programs, rates and to get approved for a mortgage.

Buying a home is very exciting. However, nothing can be a bigger disappointment than finding out that your loan is denied before you are about to close your transaction!

You’re a week away from having the keys to your new home and your loan officer calls to let you know that your loan was denied due to a change in your financial profile. This can and does happen, But there are a few things that you can do to make sure that this won’t happen to you.

Keep the following points in mind while you are in the process of buying your home:

Don’t Apply for New Credit of Any Kind. Don’t respond to any invitations to apply for new lines of credit and don’t establish new lines of credits for furniture, appliances, computers, department stores etc. Even if there are no payments for 12 months, we will need to count this debt against you. This will also have an adverse effect on your credit score. Wait until your loan closes to purchase items for yourself and new home. It is also important to limit the amount of times you have your credit pulled, as each occurrence will need to be explained.

2. Don’t Max Out or Over Charge on Existing Credit Cards. Running up your credit cards is the fastest way to bring your score down. Once you have engaged in the loan process, try to keep your credit card balances to below 30% of the available limit.

3. Don’t Close Credit Card Accounts. If you close a credit card account, it can negatively affect your FICO scores as your credit is based on History. You may have a card that is never used, but dates back 10 years and your scores do weigh heavily on this. If you really want to close an account, wait until after you close the loan.

4. Don’t Raise Red Flags to the Underwriter. Don’t change your name and address, don’t co-sign on another person’s loan. Don’t open up a new checking/savings account, make sure your taxes are filed. The less activity that occurs while your loan is in process; the better it is for you.

5. Don’t Make Large Unexplained Deposits Into Bank Accounts. Any Deposits into your bank accounts that do not match your past income history will be questionedby an underwriter unless the deposit is documented as a gift or can be explained. This includes cash deposits and moving funds from one account to another. Make sure you write your offer check from the same account you intend on writing your purchase and sales deposit. All bank accounts must be verified.

6. Don’t Make Changes to Your Employment/Income. Employment stability is a huge factor in the underwriting loan process. Quitting or changing jobs or even moving positions within the same company can greatly endanger your loan approval. Inform your loan officer immediately of any changes to your job, position or income and even the hours you work.

7. Your Down Payment: Do you have your down payment all set? Is it in one account? Have this prepared before you purchase your home. Whether it is gift funds, liquidation of your retirement or moving funds from one account to another. By having these funds all in one account, it will simplify the process. If you receive a Gift, let’s say for $1,000 from family, Don’t deposit $900 or $1100, as this will be hard to explain why the amount is different from the Gift amount. Keep it Simple!

8. Do not make any Large Purchases: If you purchase furniture with no payments for a year, banks will debt you for this. If you buy a small home in cash, banks will debt you for the taxes and insurance. College Tuition, even if the loans are deferred, banks will add this to your debts.

Bottom Line: Don’t Make Any Adjustments/Transfers in Your Financial Picture. If you even had to question your decision, make sure you talk to your loan officer first. Don’t make any changes in investments, Move your accounts or transfer, close accounts, open new accounts, or substantially alter your asset picture.

Share this with anyone you know who may be purchasing a home.

Remember, if you have a question, please call me anytime!! It may be the difference in owning your new home or being denied!!

Bill Nickerson | NMLS #4194 | (c) l 978-273-3227 | Email Me.

We

We